Protect your health and finances

Critical Illness Insurance

We'll help you get the right protection for you and your family

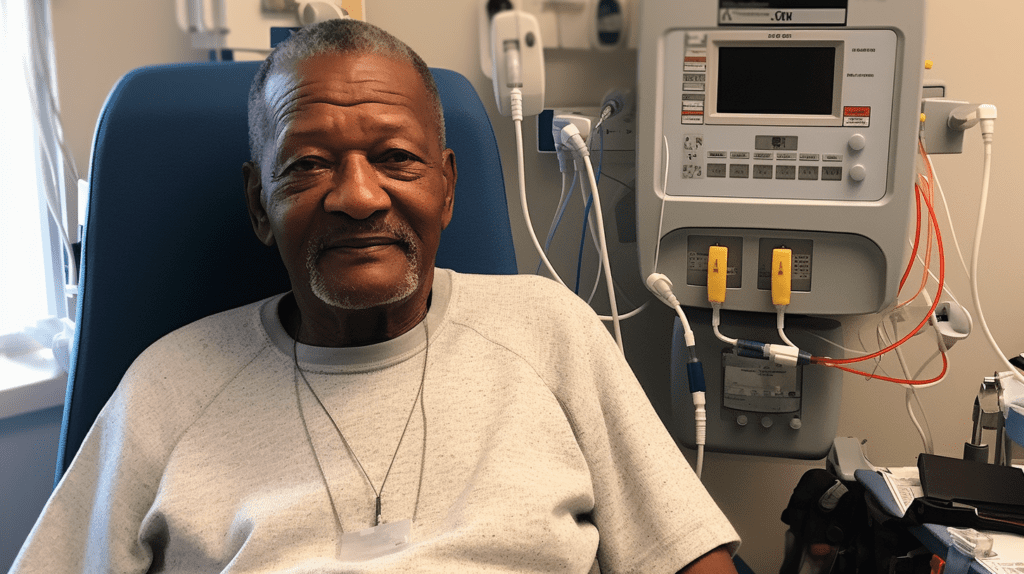

In today’s uncertain world, securing your financial future is more important than ever. Critical Illness Insurance offers peace of mind by providing a financial safety net if you’re diagnosed with a serious illness. This coverage ensures you can focus on recovery without the added stress of financial burdens.

What is critical illness insurance?

Critical Illness Insurance is a type of insurance policy that provides a lump sum payment if you’re diagnosed with a specified critical illness. This payout can be used to cover medical expenses, household bills, or any other financial obligations, allowing you to concentrate on getting better.

How does critical illness insurance work?

Key Benefits of Critical Illness Insurance

Critical Illness Insurance is essential for anyone who wants to protect their financial future. Whether you’re single, married, or have a family, this coverage can provide vital support during a difficult time.

- Customisable Plans: Tailor your policy to fit your specific needs

- Fast Payouts: Quick claims process ensures you receive funds when you need them most

- No Restrictions: Use the lump sum payment for any purpose, from medical bills to everyday expenses

Critical Illness Insurance FAQs

What illnesses are covered by Critical Illness Insurance?

Is Critical Illness Insurance the same as Health Insurance?

Can I have multiple Critical Illness Insurance policies?

How do I make a claim on my Critical Illness Insurance policy?

Is the payout from Critical Illness Insurance taxable?